Building a Better Index

Most investors don’t question how indices are built. They probably should.

The S&P 500, the Nasdaq 100 (NDX / QQQ), the Russell indices—nearly all of the most widely followed benchmarks—are market-cap weighted. The larger a company’s market capitalization, the larger its weight in the index. Simple. Clean. Objective. And in our view, deeply flawed.

The Problem with Market-Cap Weighting

Market-cap weighting assumes that bigger automatically means better. The more a stock has gone up in the past and the larger its market cap grows, the index allocates a higher percentage of capital to it going forward.

That works well sometimes. But it also creates structural issues:

Stocks become largest after they’ve already performed well

Capital is allocated based on size, not future potential

Concentration risk quietly builds at market extremes

Index exposure becomes increasingly backward-looking

In short, market-cap weighting optimizes for what was, not what will be.

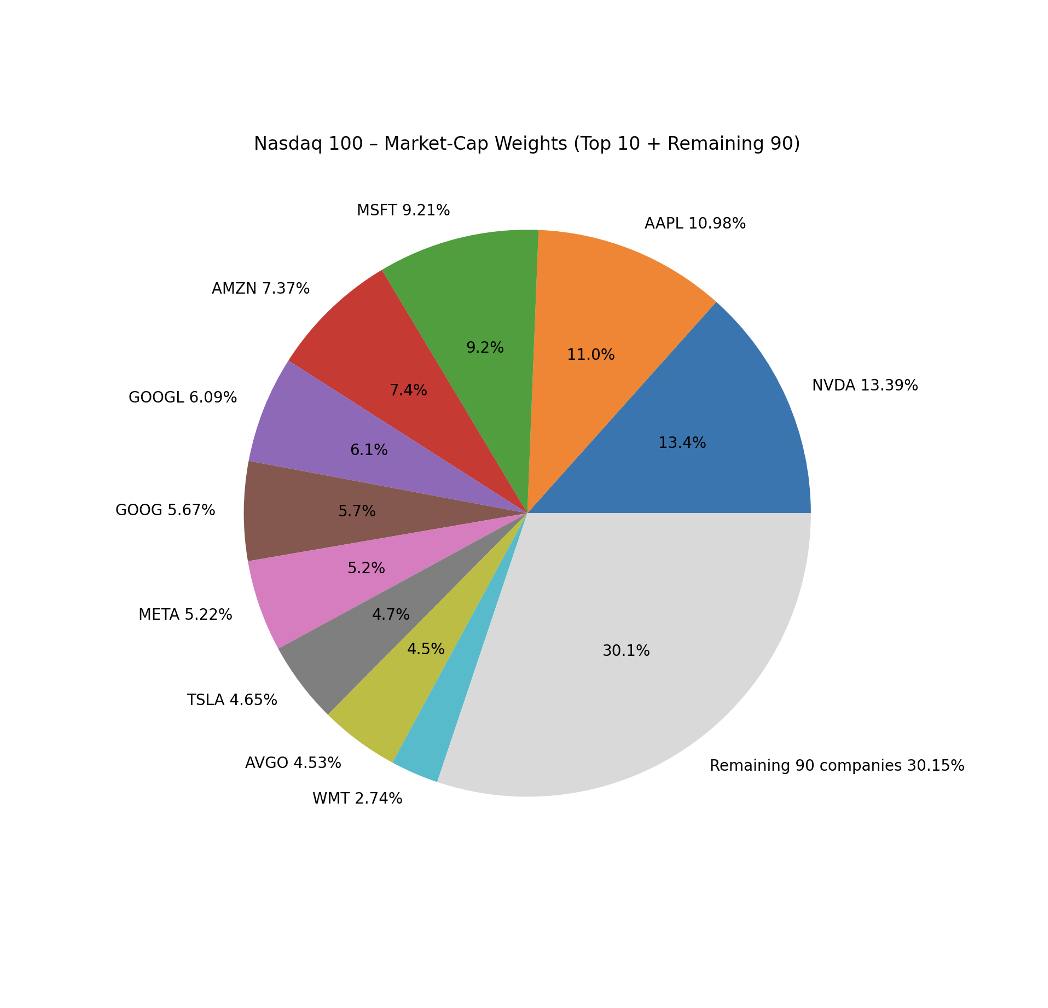

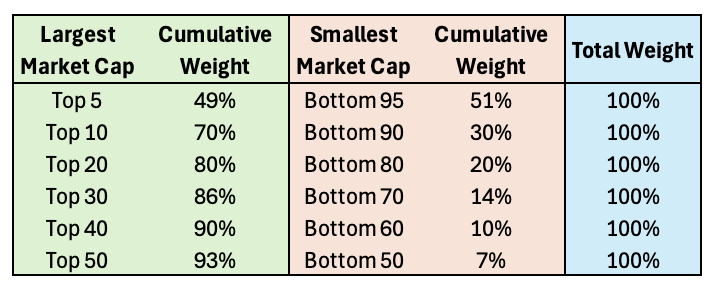

Nasdaq 100 - Market-Cap Weights (Top 10 + Remaining 90)

Source: https://www.slickcharts.com/nasdaq100 as of Feb 1, 2026.

Viewed differently, the lower-weighted half of the Nasdaq 100 contributes minimally to aggregate index returns, despite the fact that many of these companies exhibit strong growth characteristics, compelling products and services, and the potential for significantly greater price appreciation relative to their mega-cap peers.

A Simple Analogy: Coaching a Football Team

Imagine you’re offered the head coaching job of one of two football teams.

On Team A, the rules are simple—but rigid.

You must weigh every player. The heaviest player starts at the first position. The second heaviest starts at the second position. And so on, until all 11 positions are filled. This approach might work reasonably well for centers and guards. But what about the quarterback? The running backs? The wide receivers? Size alone does not determine effectiveness at every position.

On Team B, the rules are different.

You can evaluate each player based on their skill set, their role, and how you expect them to perform in that specific position.

Which team would you rather coach? We’d choose Team B every time.

Indices Are No Different

Market-cap weighting is Team A.

It forces the largest stocks—by price appreciation and capital inflows—to dominate index exposure regardless of whether they are best positioned to perform going forward.

A better approach is to acknowledge a simple truth: Different companies contribute differently to future returns. Some deserve larger roles. Some deserve smaller ones. And some deserve to sit on the bench—at least for now.

Introducing a Better Framework

This philosophy is exactly the framework we are developing for a new product currently in design — one that holds the same constituents as the Nasdaq 100 but weights them based on forward-looking potential rather than market cap.

The product will hold the exact same constituents as the Nasdaq 100. Same companies. Same universe. No stock picking outside the benchmark. The difference lies entirely in how those companies are weighted. Instead of allocating capital based on market capitalization, we will weight constituents based on how we believe they are positioned to perform going forward—considering factors such as business momentum, structural tailwinds, and risk-reward asymmetry. In other words, we’d rather be the coach who builds a lineup based on ability and fit, not just size.

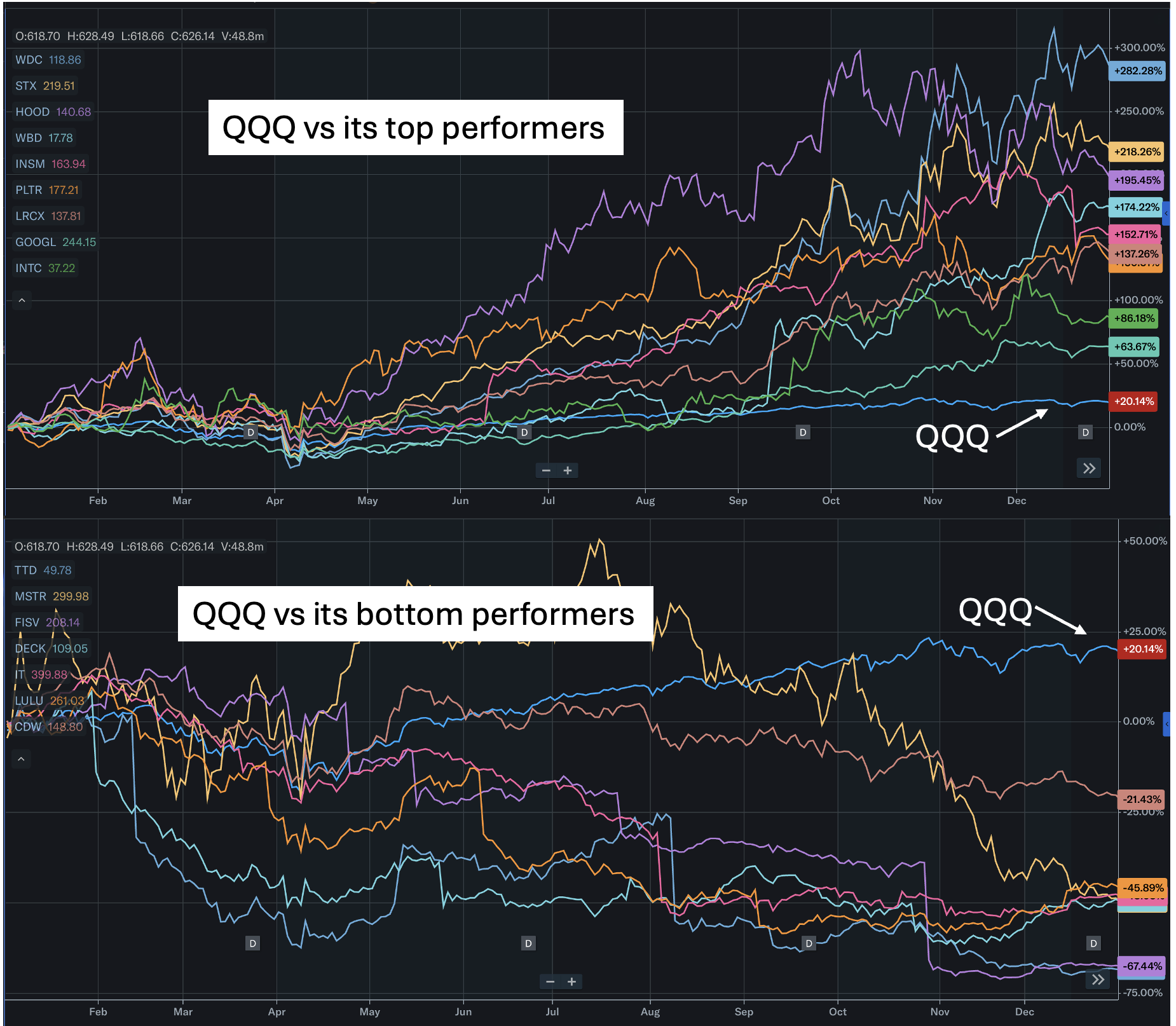

Illustration of QQQ top performing constituents vs bottom performing

The Goal Isn’t Complexity—It’s Intentionality

This isn’t about making indices complicated. It’s about making them purposeful. Market-cap weighting is easy. Thoughtful weighting is harder. But just like coaching, investing isn’t about following the simplest rule—it’s about making the best decisions with the information available. We don’t believe size alone should determine importance. And we don’t believe yesterday’s winners should automatically dominate tomorrow’s portfolio. That’s why we set out to build a better index. So the real question isn’t whether market-cap weighting is simple—it’s whether it’s the best way to allocate capital going forward.

Our View

Market-cap-weighted indices are not wrong—they are simply backward-looking.

They are easy to construct, easy to maintain, and easy to understand. But simplicity comes at a cost. By design, these indices allocate the most capital to stocks that have already become the largest, not necessarily to those with the most attractive future risk-reward. By allocating capital based purely on size, traditional indices systematically overweight yesterday’s winners and underweight tomorrow’s opportunities.

We believe index construction should be intentional, not rigid.

In our view, indices should not be built by blindly lining up the heaviest players. They should be built by putting the right players in the right positions.